Vehicle Repossession in Oregon

Understanding Vehicle Repossession in Oregon

Facing the possibility of losing your car is a high-stress experience that can leave you feeling stranded—both literally and financially. In Oregon, lenders hold significant power when it comes to vehicle repossession. If you default on your auto loan or lease, the law generally allows creditors to take back the property used as collateral.

Most people associate "default" with several missed payments, but in reality, a default can occur the moment you are a single day late, fail to maintain required insurance, or violate a specific term in your lease agreement. Navigating Oregon vehicle repossession laws is complex, but understanding your rights is the first step toward protecting your transportation and your financial future

Oregon Laws and Regulations on Vehicle Repossession

Oregon’s legal framework for repossession is primarily governed by the Uniform Commercial Code (UCC) and specific Oregon Revised Statutes (ORS). Unlike some other states that require a court order for most seizures, Oregon allows for "self-help" repossession.

Under ORS 79.0609, a secured party may take possession of the collateral after a default without judicial process, provided they do not "breach the peace." This means the lender does not have to warn you before the tow truck arrives. However, they cannot use physical force, enter a locked garage without permission, or threaten you during the process.

The Repossession Process

The journey from a missed payment to an empty driveway typically follows a specific legal trajectory in Oregon:

1.Loan Default: The process triggers the moment you breach your contract. While some lenders offer a grace period, Oregon law does not mandate one for standard auto loans.

2.Repossession: A repossession agent can seize the vehicle from a public street or your driveway at any time of day or night. If you catch them in the act and tell them to stop, they are generally required to leave to avoid "breaching the peace," though they will likely return later.

3.Post-Repossession Notification: Per ORS 79.0611, the lender must send you a written notice after the car is taken. This letter must explain your right to get the car back and provide details about the upcoming sale.

4. Sale of the Vehicle: The lender will usually sell the car at a private sale or public auction. They are legally required to conduct this sale in a "commercially reasonable" manner to ensure the highest possible price is fetched.

Notice Requirements and Communication with the Lender

While Oregon doesn't require a pre-repossession warning, the post-repossession notice is a critical legal requirement. This document must include:

- An itemized list of what you owe (the "payoff" amount).

- The date, time, and location of the public auction, or the date after which a private sale will occur.

- A description of your liability for a "deficiency balance."

Maintaining open lines of communication with your lender before the tow truck arrives is always the best strategy. Lenders often prefer receiving partial payments over the high cost of seizing and selling a vehicle.

Preventing Vehicle Repossession in Oregon

If you see the writing on the wall, don't wait for the vehicle to disappear. Proactive measures can often save your credit and your car. You might consider:

- Requesting a Deferral: Many lenders allow you to move one or two payments to the end of the loan term.

- Changing the Due Date: If your pay schedule has shifted, a simple date change can prevent future defaults.

- Filing for Bankruptcy: This is the most powerful tool available. Filing for bankruptcy triggers an "automatic stay," which legally bars lenders from repossessing your vehicle immediately.

Loan Modification and Refinancing

For those with a steady but lower income, modifying the existing loan or refinancing with a new lender can provide much-needed breathing room.

Benefits:

- Lower Monthly Costs: Extending the loan term can drop your monthly obligation significantly.

- Interest Rate Reduction: If your credit has improved since you bought the car, refinancing can save you thousands in interest.

Drawbacks:

- Total Cost: Extending a loan term means you will pay more interest over the life of the loan.

- Upside Down: You may end up owing more than the car is worth (negative equity).

Voluntary Repossession and Its Implications

If you simply cannot afford the car, you can choose "voluntary surrender." This involves calling the lender and arranging a time to drop the vehicle off.

Pros:

- Reduced Fees: You avoid the expensive towing and storage fees associated with a forced repo.

- Less Conflict: It is a controlled process that avoids the embarrassment of a surprise seizure.

Cons:

- Credit Damage: It still shows up as a "voluntary repossession" on your credit report, which is nearly as damaging as an involuntary one.

- Deficiency Balances: You are still responsible for the difference between the sale price and your loan balance.

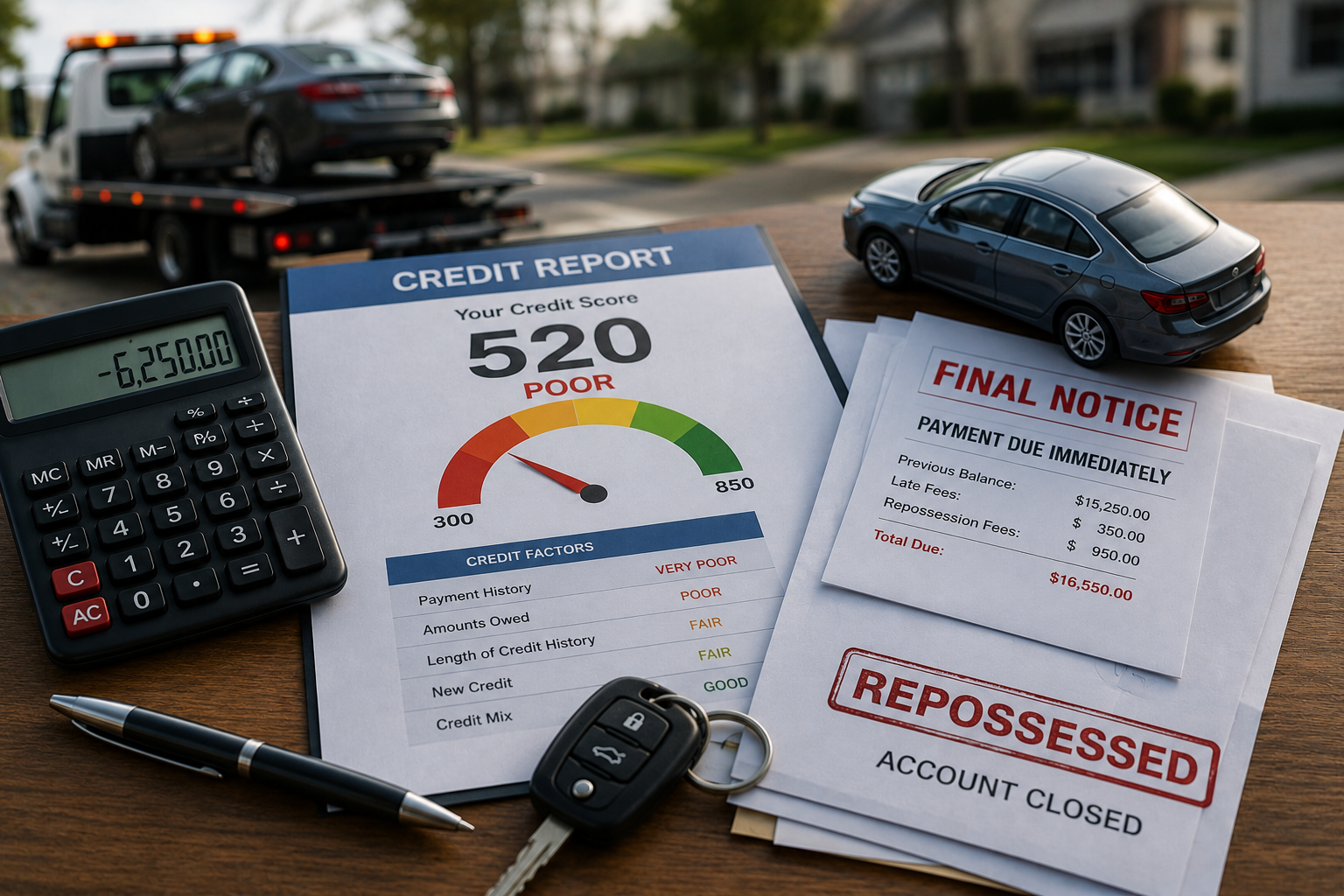

Consequences of Vehicle Repossession in Oregon

The loss of the car is often just the beginning of the financial fallout.

- Credit Score Impact: A repossession can stay on your credit report for seven years, significantly lowering your score and making future borrowing (including for housing) much more difficult.

- The Deficiency Balance: If you owe $15,000 and the car sells at auction for $9,000, the lender will likely sue you for the remaining $6,000, plus repossession fees.

- Legal Action & Garnishment: If the lender wins a deficiency judgment in an Oregon court, they can garnish your wages or levy your bank accounts.

Rebuilding Your Credit After a Vehicle Repossession

Recovery is possible, but it requires a disciplined approach.

- Address the Deficiency: If possible, negotiate a settlement for the remaining balance so it shows as "paid" on your report.

- On-Time Payments: Ensure every other bill—rent, utilities, and credit cards—is paid on time.

- Credit Monitoring: Use tools to watch your score and ensure the lender is reporting the repossession accurately according to the law.

Getting Your Vehicle Back After Repossession in Oregon

Under Oregon vehicle repossession laws, you generally have two paths to reclaim your car:

- Redemption: This requires paying the entire loan balance plus all repossession costs. This is often difficult for someone already in financial distress.

- Reinstatement: Oregon law does not strictly require lenders to allow "reinstatement" (paying only the past-due amount), but many contracts allow for it. You must check your specific loan agreement.

- Chapter 13 Bankruptcy: This allows you to "cure" the default over a 3-to-5-year period. In many cases, if you file quickly enough, you can even force the lender to return a vehicle they have already seized.

Participating in Repossession Auctions

You have the legal right to bid on your own vehicle at a public auction. While this might seem like a way to buy the car back for less than the loan amount, it is risky. If you are the winning bidder, you still owe the deficiency balance (the difference between your bid and the original loan amount).

Get in Touch With an Attorney

If you are struggling with car payments or have already lost your vehicle, time is of the essence. At our firm, we specialize in helping Oregonians navigate the intersection of vehicle repossession and bankruptcy law. We can help you determine if a Chapter 7 or Chapter 13 filing is the right path to stop the repo man, eliminate your debt, and keep you on the road.

Contact us today for a consultation to protect your rights and your transportation.

Oregon Vehicle Repossession FAQ's

Can personal belongings inside my repossessed vehicle be kept by the lender?

No. In most cases, the lender cannot permanently keep your personal property. You generally have the right to retrieve personal items left inside the vehicle, although there may be deadlines or storage fees involved.

Do lenders have to notify me before selling my repossessed car?

Yes. Oregon law generally requires lenders to send notice before the vehicle is sold. This notice should explain the sale process and provide information about your rights and any remaining debt.

What happens if the repossession company damages my property during the process?

If a repossession agent damages your property or violates the law during the repossession, you may have legal grounds to pursue compensation. This can include damage to a garage, driveway, gate, or other personal property.

Share On: